The 401(k) remains the cornerstone of retirement planning for millions of Americans. Yet simply enrolling isn’t enough—maximizing this tax-deferred vehicle requires intentional asset selection. In 2025, with elevated market valuations, persistent inflation, and evolving interest rate dynamics, the best 401(k) investments balance growth, diversification, and cost efficiency to compound wealth over decades—not chase short-term trends.

Core Principles for 401(k) Allocation

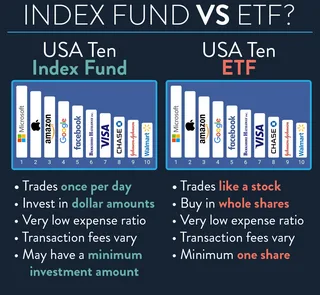

- Prioritize Low-Cost, Broad-Market Index Funds

The foundation of any strong 401(k) should be low-expense-ratio index funds that offer instant diversification. Look for options like:- U.S. Total Stock Market (e.g., Fidelity ZERO Total Market or Vanguard Institutional Index)

- International Developed Markets (e.g., MSCI EAFE index fund)

- U.S. Aggregate Bond Market (e.g., Bloomberg U.S. Aggregate Bond Index fund)

- Avoid Overconcentration in Company Stock or Sector Funds

Holding more than 10% of your 401(k) in employer stock dramatically increases idiosyncratic risk (as Enron and Silicon Valley Bank retirees learned). Similarly, speculative sector bets (e.g., “AI Only” or “Crypto Adjacent” funds) lack diversification and long-term stability. - Use Target-Date Funds Wisely—But Audit Their Holdings

Target-date funds (e.g., “2060 Fund”) offer automatic glide-path rebalancing and are suitable for hands-off investors. However, review their underlying allocations: some overweight high-fee active managers or underweight international exposure. Opt for those with >80% in low-cost index vehicles.

Maximizing Tax Deferral: What Goes Where

Because 401(k)s are tax-deferred (not tax-free), they’re ideal for holding assets that generate ordinary income—like bonds or REITs—which would be taxed annually in a taxable account. Conversely, high-growth, low-dividend stocks are better suited for Roth accounts where gains compound tax-free.

When to Go Beyond the Menu

If your plan offers fewer than five core funds or charges high fees (>0.50% on passive options), consider:

- Contributing enough to get the full employer match (free money), then directing excess savings to a Roth IRA or taxable brokerage with better investment choices

- Advocating for plan improvements through your HR department—many providers now offer institutional share classes at near-zero cost

Conclusion

The best 401(k) investments aren’t flashy—they’re simple, diversified, and cost-conscious. In 2025, disciplined allocation within this tax-advantaged structure remains one of the most reliable paths to retirement security.

For institutional guidance on long-term wealth strategies beyond retirement accounts, learn more at valuefinity.com or reach us at Capital@valuefinity.com .