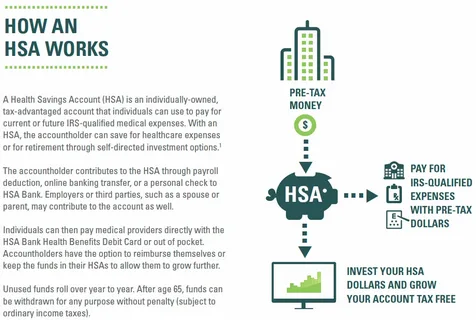

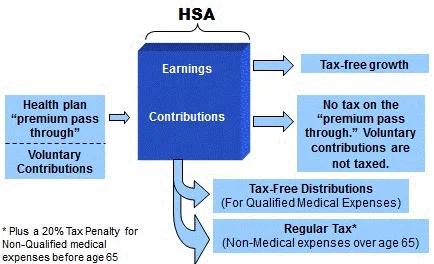

The Health Savings Account (HSA) is the most tax-advantaged investment vehicle in the U.S.—offering triple tax benefits:

- Tax-deductible contributions

- Tax-free growth

- Tax-free withdrawals for qualified medical expenses

Yet most HSA holders leave their funds in low-yield cash, missing a powerful opportunity. For those with stable health coverage and the ability to pay current medical bills out of pocket, the best investments for an HSA treat it like a long-term growth account—not just a medical expense buffer.

When to Invest Your HSA (Not Just Save)

If you can cover routine healthcare costs from your checking account, consider investing your HSA once you’ve built a cash reserve for emergencies (typically $1,000–$3,000, depending on your deductible). Everything above that threshold can be invested for decades of tax-free compounding.

Best Investment Options for an HSA in 2025

- Low-Cost, Diversified Index Funds

Most HSA providers (e.g., Fidelity, Lively, Health Savings Administrators) offer brokerage-linked HSAs. Allocate to:- U.S. total stock market ETF (e.g., FZROX or VTI) – core holding

- International developed markets ETF (e.g., VXUS) – for diversification

These funds have expense ratios near 0.00%–0.03% and automatically reinvest dividends—maximizing compounding.

- Dividend-Growth Stocks (for Later-Life Medical Funding)

As you near retirement, consider shifting a portion into high-quality dividend growers (e.g., Johnson & Johnson, UnitedHealth). These provide income to cover rising healthcare costs without selling shares in down markets. - Target-Date Funds (for Hands-Off Investors)

If you prefer automation, choose a low-cost target-date fund (e.g., Fidelity Freedom Index 2060) that gradually shifts from growth to income as you age—ideal for “set-and-forget” HSA investing.

- Leaving all funds in cash: With inflation averaging 3%+, cash loses ~30% of its purchasing power per decade.

- High-fee mutual funds: Some HSA platforms charge 0.50%+—eroding long-term returns. Stick to low-cost ETFs.

- Speculative assets: Avoid individual stocks, crypto, or sector bets—this isn’t the place for risk.

The Strategic Payoff: Healthcare as a Retirement Expense

Fidelity estimates the average 65-year-old couple will spend $300,000+ on healthcare in retirement (not including long-term care). An invested HSA can cover these costs tax-free—making it a stealth retirement account. And after age 65, you can withdraw for any reason (penalty-free, taxed as income)—adding flexibility.

Conclusion

The best investments for an HSA in 2025 leverage its unmatched tax structure to build long-term health security. By treating your HSA as a 20- to 30-year growth vehicle, you turn today’s medical savings into tomorrow’s care—with zero tax drag.

For guidance on integrating HSA strategy into a broader institutional-grade wealth plan, visit valuefinity.com or reach us at Capital@valuefinity.com .